- Following the Fed’s 75 basis point rate hike and related commentary, US Treasury yields beyond two years rallied significantly based on concerns about economic growth and market participants recalibrating expectations of future rate moves. The market is now anticipating that the Fed will begin cutting rates next year and is increasingly concerned about recession, as evidenced by the inversion between the 2 Year and 10 Year Treasury yields.

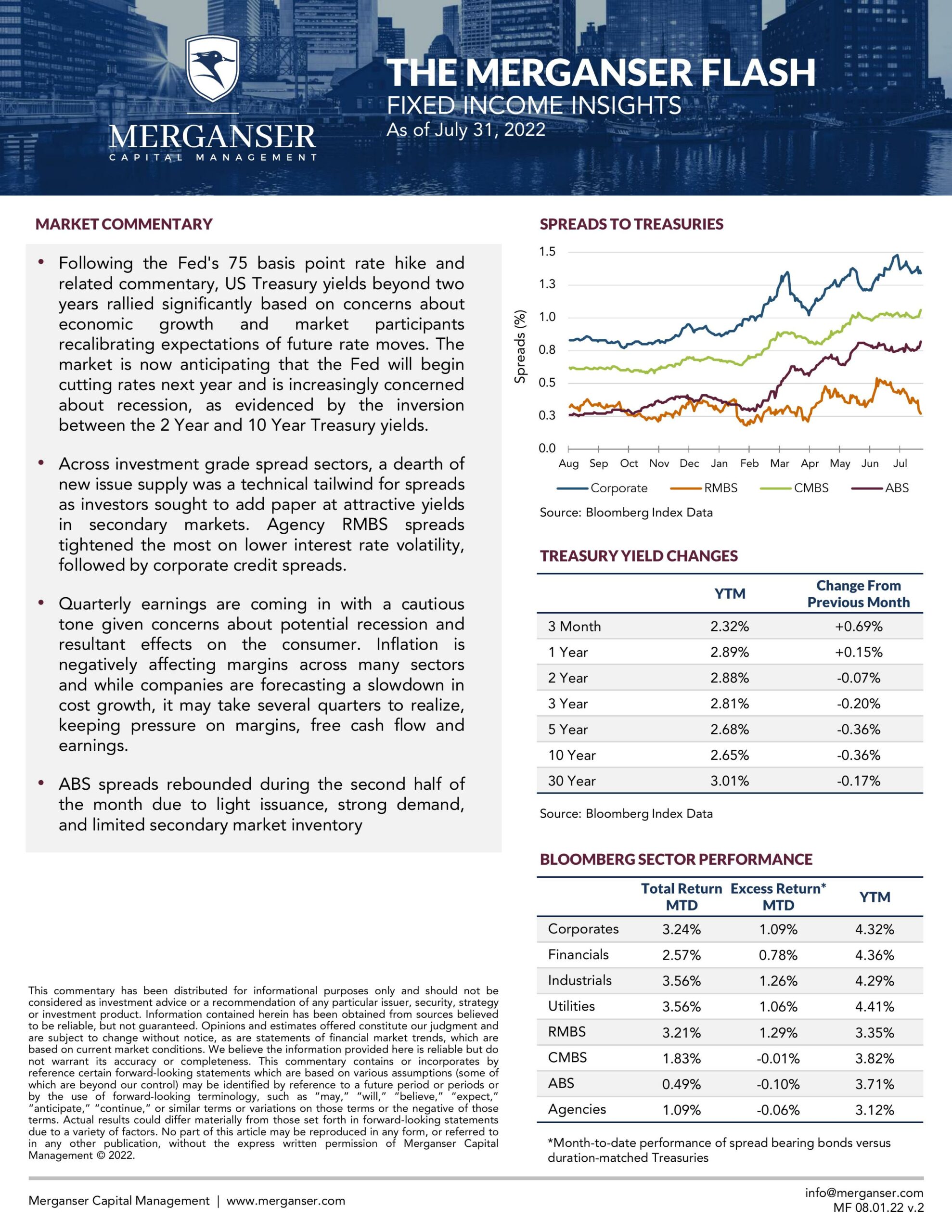

- Across investment grade spread sectors, a dearth of new issue supply was a technical tailwind for spreads as investors sought to add paper at attractive yields in secondary markets. Agency RMBS spreads tightened the most on lower interest rate volatility, followed by corporate credit spreads.

- Quarterly earnings are coming in with a cautious tone given concerns about potential recession and resultant effects on the consumer. Inflation is negatively affecting margins across many sectors and while companies are forecasting a slowdown in cost growth, it may take several quarters to realize, keeping pressure on margins, free cash flow and earnings.

- ABS spreads rebounded during the second half of the month due to light issuance, strong demand, and limited secondary market inventory