- US Treasury yields continued their ascent higher during August in response to stronger than expected employment data and commentary from Fed Chair Powell confirming that the Fed is committed to taming inflation, even if doing so may cause economic harm.

- July CPI data in the US came in below expectations, suggesting that scorching levels of inflation may be in the “early innings” of cooling.

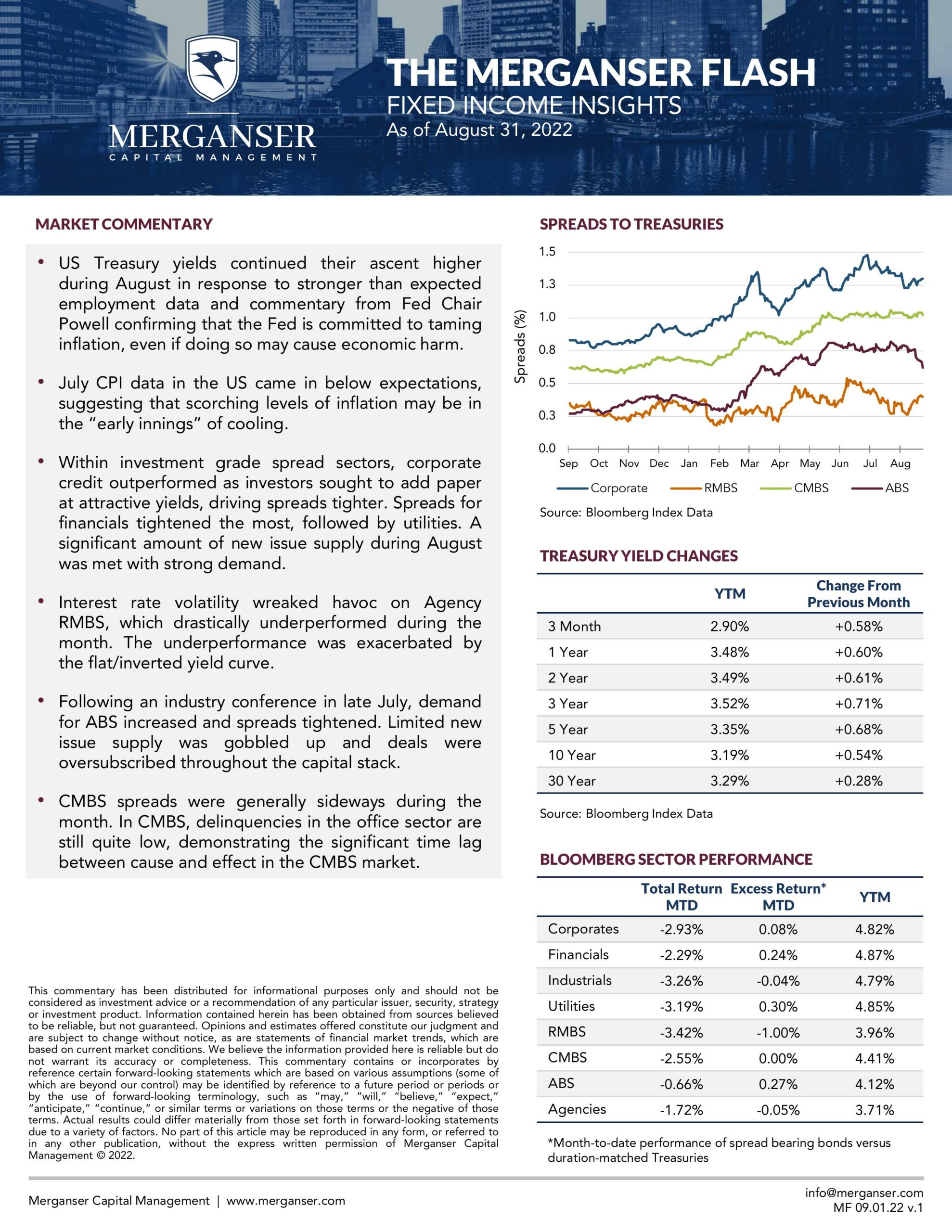

- Within investment grade spread sectors, corporate credit outperformed as investors sought to add paper at attractive yields, driving spreads tighter. Spreads for financials tightened the most, followed by utilities. A significant amount of new issue supply during August was met with strong demand.

- Interest rate volatility wreaked havoc on Agency RMBS, which drastically underperformed during the month. The underperformance was exacerbated by the flat/inverted yield curve.

- Following an industry conference in late July, demand for ABS increased and spreads tightened. Limited new issue supply was gobbled up and deals were oversubscribed throughout the capital stack.

- CMBS spreads were generally sideways during the month. In CMBS, delinquencies in the office sector are still quite low, demonstrating the significant time lag between cause and effect in the CMBS market.